Monthly Archives: March 2020

Precedent for Unprecedented Times

With the recent swings in the market, we wanted to provide a new update on what we are seeing in the market and the economy. This week has seen some strong returns, particularly on Tuesday, when the S&P 500 index posted its eighth-highest daily return in history at 9.38%. Individuals may be feeling like a day as strong as this is proof that the worst of this crisis is behind us, and we would love that to be true. However, we would like to provide some historical context and precedent in these unprecedented times.

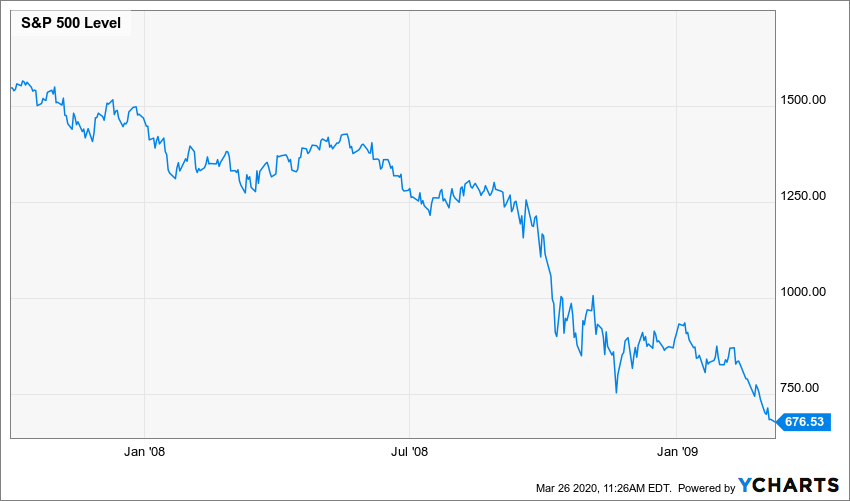

As was previously mentioned, there have only been seven days in the S&P’s history in which the market posted a greater daily return than the one we saw on Tuesday. In order from largest to smallest, these other seven days happened in 1933, 1929, 1931, 1932, twice in October 2008, and 1939. Anyone familiar with history will recognize that, yes, the largest up days in market history happened during the Great Depression and Great Recession, which can seem counterintuitive. The two modern-day examples in October 2008 are an interesting case study. On October 13, 2008, the S&P 500 posted a return of 11.58%. If you were an investor who started to feel FOMO (Fear of Missing Out) about potentially missing the beginning of the next bull market and entered the market after this day, you would have experienced a decline of over -32% after this day. In fact, as soon after as October 22, 2008, the market was setting a new low. On October 28, 2008, the S&P 500 had a return of 10.79%. Now, if you refused to act on the first large up day but saw this day as confirmation, you would have experienced a decline of roughly -28% before the market bottomed out on March 9, 2009. While this isn’t to guarantee that we will see this sharp of a decline after Tuesday’s strong day, it does tell us that these days are far from a signal that we are out of the woods.

Also, another aspect of recessionary drawdowns is continual fluctuations off the bottom before setting new lows. We decided to look at the past two recessions, as well as the crash of 1987 to see if there is a precedent for these kinds of upswings during bear markets. In 2008, the S&P 500 had five separate instances where the index was 10% or more off the bottom before pulling back and setting a new low. In fact, on January 6, 2009, the S&P 500 was over 24% off the bottom before losing these gains in the following two months. In 2000, the S&P 500 once again had five separate occasions where the index was over 10% off the bottom before setting new lows shortly thereafter.

On January 4, 2002, the market was over 21% off the bottom before pulling back -33.75% afterwards. Lastly, even a crash as fast as Black Monday saw the market over 10% off the bottom before pulling back and setting a new low a little over a month later. As of Wednesday’s close, the S&P 500 is now 10.64% off the bottom. While these improvements are a welcomed sight, history has shown us that the market simply having upturns during bear markets is not unprecedented and typically isn’t an end-all signal that it is time to enter the market again.

Now that we have discussed precedent for these situations, let’s discuss some of the unprecedented events happening today. Today it was announced that unemployment claims last week were 3.28 million, which not only is nearly five times the previous record high from 1982, but it is also much higher than the consensus estimates of 1.5 million by economists surveyed by Dow Jones. Also, recent estimates by some of the largest banks are projecting U.S. GDP (a measure of the amount of goods and services produced in the U.S.) to decline anywhere from -14% to -30% in the second quarter of this year, in no small part due to the social distancing and quarantines we have seen. While these levels are unprecedented, the hope would be that this kind of a contraction will be short-lived. However, with many service industry employees (particularly in restaurants and entertainment) being laid off, it is difficult to exactly project how this recovery will take shape.

While we are experiencing both unprecedented and precedented times during this crisis, one crucial aspect regarding investing is to stay the course. More than half of our recession indicators continue to maintain a negative reading, which means that we suggest remaining on the sidelines for now. When we begin to see strength return to these indicators, we will begin our reintroduction into the market. However, we have yet to see any material improvement in any of the indicators, even after Tuesday’s upswing. In fact, none of the indicators through 2000 and 2008 fell for any of the false 10% upswings; the indicators only began gaining real strength when the recessions were truly finished. Remember, a math-based process can remove the two most dangerous emotions for an investor: fear and greed. In the past, we have cautioned against reacting fearfully during corrections, but we also want to caution against reacting with greed when it comes to entering the market again; a buy discipline is just as crucial to an investment process as a sell discipline. We will continue to monitor things daily to see if this week’s movement is another historical head fake, or if it is a sign of strength returning to the market. In the meantime, if you have any questions or concerns, don’t hesitate to reach out.

Thank you,

Bud Verfaillie and Ashley Rosser

Bud Verfallie, CEO

Bud Verfallie, CEO

Bud holds several professional designations including: AIFA (Accredited Investment Fiduciary Analyst/Center for Fiduciary Studies), PPC (Professional Plan Consultant/Financial Service Standards), and CFP (Certified Financial Planner/College of Financial Planning), ranking him in the top 1% of all Investment Consultants nationally.

Bud has been an instructor/trainer for over 25 years. Subjects include: “How to Initiate a Successful Asset Management Business in Your Accounting Firm”, “Converting Your Commissioned-Based Investment Practice to Fee-Based”, “How to Establish an Asset Management Practice”, and “Investments and Financial Planning.” Bud has taught financial planners CFP Preparatory classes for the NIF.

Ashley Rosser, President

Ashley Rosser, President

Prior to her career in the financial services industry, Ashley earned her Bachelor of Science in Nursing from Cedarville University.

Ashley decided to make a career change from her ten years within the healthcare industry as a pediatric emergency room nurse to retirement and 401K investment planning. She joined Victory Wealth Partners in 2008 after obtaining her Series 65 professional financial license and went on to earn her AIF (Accredited Investment Fiduciary) professional designation from the Center for Fiduciary Studies.

The opinions voiced on this website are for general information only and are not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and not be invested into directly. The Standard & Poor’s 500 Index is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

Why We Went to Cash – Market Indicators

This article was hard for me to write this month. It almost seems trivial to write about financial matters when we are worried about our families staying safe and our businesses remaining open. When COVID-19 is over medically, we know we will have to assess the damage done financially. I do not take any of this lightly.

Click Here for a Recent Update >>>

I think there are important questions that investors should be asking right now. I wanted to share what our firm did for our clients and why it may be appropriate for you.

We went to cash. Yep. You read that right. We sold all our equity positions in the market. I know your saying “but that goes against everything my advisor is telling me to do”. Yes, we know. If you have been following my blogs, you may recall that we use a math-based program to help us determine how we should be invested. Our Investment Committee is comprised of five firms from across the nation which utilizes the same math-based program, and it has been around for over 30 years. The first question we answer is, should we be in the market or be in cash to preserve principal? Since May 2009, stocks have been the best place to be. All that began to change three weeks ago.

We track six indicators that help determine the overall strength of the stock market. When a majority are positive, we remain in the market. If 4 or more go negative, it is a sign that there are significant technical and fundamental underlying deficiencies in the market. The indicators are not affected by short-term volatility.

Initially, we observed minimal changes as the volatility was related to fear sell off and not underlying issues. But, as companies, industries, states and entire countries shut down, those indicators were changing rapidly. On March 12th, three indicators went negative, then another two on March 17th, meaning that five of our six indicators were negative. Our Investment Committee made the important decision to move all positions to either a government guaranteed money market or a stable value fund. These indicators also went negative in 2000 and 2008. The point is we have a stop loss in place that seeks to stop any further losses until conditions improve. Government stimulus packages will probably provide a temporary market uptick, but will have little impact on the underlying fundamentals and our indicators. In a market decline, think of a person walking down the steps with a yo-yo. The yo-yo goes up and down as the person is walking down the steps but the overall trajectory is still downward.

We also have a buy discipline. As our indicators begin to turn positive again, we will tactically transition by adding specific asset classes and sectors as appropriate. There will be a significant investment opportunity when that happens.

Our decision was not emotional but based on a very methodical process. These are the questions you need to ask. What is your sell discipline? When was the last time it was executed? How effective was it? Your buy discipline is just as important. If you do go to cash to preserve your principal and do not know when to enter back in the market, you may miss one of the most opportunistic times in history. If you are not encouraged by the answers, it may be time for a second opinion.

This month’s topic is definitely heavier than what I normally post, but given our current circumstances I felt it was necessary. If you would like further information on our investment methodology, I am happy to send you over a webinar that was recorded for all our clients. It gives an overview of the data that we used to help our decision-making process. We are willing to share it with you .

In closing, I would like to reiterate our hope for you and your family to remain healthy. I will be praying for all the small businesses in our community who are undoubtedly feeling the strain of social distancing policies. The United States will survive and when we come back, we will be stronger than before. We are here to help support our friends and neighbors however we can in the coming days and weeks. We are in this….together.

Ashley Rosser, President

Prior to her career in the financial services industry, Ashley earned her Bachelor of Science in Nursing from Cedarville University.

Ashley decided to make a career change from her ten years within the healthcare industry as a pediatric emergency room nurse to retirement and 401K investment planning. She joined Victory Wealth Partners in 2008 after obtaining her Series 65 professional financial license and went on to earn her AIF (Accredited Investment Fiduciary) professional designation from the Center for Fiduciary Studies.

The Current Health of the Economy During the COVID-19 Outbreak

While reaction to the Coronavirus COVID 19 continues to remain top of mind, we want to bring attention to the current health of the economy. Generally speaking, we believe there are four different triggers that tend to lead to recession.

The health of the economy in four indicators

The first trigger we look at is unemployment. Just last Friday, it was announced that unemployment fell to 3.5%. In fact, the Labor Department reported that there were 273,000 new jobs in February, nearly 100,000 more than the anticipated number of 175,000.

The second trigger we look for is whether the Federal Reserve’s policy is too tight. When we say that the Federal Reserve’s policy is “tight,” this just means that they are raising interest rates to combat inflation. Currently, the Federal Reserve is loose, as they cut rates by 0.50% on Tuesday, in an attempt to curtail any short-term economic impact from the COVID 19.

The third trigger is overvalued stocks, as it may imply a bubble has formed. In 1999 before the Dot Com Bubble, the Price-to-Earnings ratio (a ratio used to measure stock valuation) for the S&P 500 index was 30.8. Today, this ratio is 22.2, well below the valuations we saw at the turn of the century.

Lastly, the final trigger is geopolitical risk. In a previous piece we wrote on February 5th, we observed every epidemic since 1950 in which there were at least 100 deaths. While one death is one too many from these epidemics, we wanted to objectively analyze how the markets have reacted to each of them. As a recap, the market saw positive returns in the 90, 180, and 365-day periods following the outbreaks, implying that they tend to have little impact on the markets in the intermediate term. In short, none of these four triggers are currently showing weakness.

As we have mentioned in previous articles, movement in the market is typically driven by one of three things: fundamentals, technical analysis, and emotion. Fundamentals in the health of the economy are still sound, with unemployment matching 50-year lows and the economy continuing to beat job growth projections. While supply chains will be affected in the short-term as companies adjust to supply shortages and shipment delays, we don’t believe there will be a long-term impact on these companies. While second and third quarter growth may show an impact, we believe that this will be a temporary decline as opposed to a prolonged issue. On the technical analysis side, our recession indicators continue to remain positive. As a refresher, these indicators would have caused us to exit the market in December of 2000 and July of 2008, well before the worst of each of those recessions. However, these were the only two times in the past 20 years that our indicators would have shown a negative reading. In fact, every indicator was positive through the 2018 correction that saw the S&P 500 fall 19.78%. Sure enough, it was a correction and we recovered with a strong 2019. While we can’t guarantee the same will happen this time, none of the indicators have shown weakness. Lastly, emotional overreaction can drive the markets. Since both the fundamentals and technical indicators are showing strength, we are inclined to believe that this is the driving force behind this market correction.

Like we mentioned in “A History of Market Corrections,” market corrections are a healthy part of investing, as they prevent the stock market from becoming overinflated in value after periods of rapid growth (like the growth we saw in the fourth quarter of 2019). Market corrections historically occur an average of every eight months, and they typically include a catalyst that causes it. In 2010, it was Greece requiring a bailout. In 2015, it was slowing Chinese economic growth. Today, it is a fear of how supply chains will be interrupted due to the Coronavirus COVID 19. It can be difficult to remain disciplined in volatile times, but that is what we strive to do at Victory Wealth Partners. We will continue to analyze the health of the economy and market daily, and we will inform you if we see any material changes in market conditions. However, since we have yet to see any changes, we will continue to stay the course. Volatile times remind us of a letter written by Dean Witter on May 5, 1932:

“Dear Clients, All of our customers with money must someday put it to work-into some revenue producing investment. Why not invest it now, when securities are cheap? Some people say they want to wait for a clearer view of the future. But when the future is again clear the present bargains will have vanished. In fact, does anyone think that today’s prices will prevail once full confidence has been restored? Let us face it-these bargains exist only because of terror and distress. And when the future is assured, the dollar will have long since lost its present buying power. It takes courage, of course, to be optimistic about our country’s future when nearly everyone is pessimistic. But it is cowardly to assume that the future of the United States is in peril.“

It can feel unnatural to be greedy when others are fearful, and it can feel unnatural to be fearful when others are greedy. However, following this old adage has been a sound guide through market history. Stay strong, stay disciplined, and don’t hesitate to reach out if you have any questions or concerns.

Bud Verfallie, CEO

Bud holds several professional designations including: AIFA (Accredited Investment Fiduciary Analyst/Center for Fiduciary Studies), PPC (Professional Plan Consultant/Financial Service Standards), and CFP (Certified Financial Planner/College of Financial Planning), ranking him in the top 1% of all Investment Consultants nationally.

Bud has been an instructor/trainer for over 25 years. Subjects include: “How to Initiate a Successful Asset Management Business in Your Accounting Firm”, “Converting Your Commissioned-Based Investment Practice to Fee-Based”, “How to Establish an Asset Management Practice”, and “Investments and Financial Planning.” Bud has taught financial planners CFP Preparatory classes for the NIF.

Ashley Rosser, President

Prior to her career in the financial services industry, Ashley earned her Bachelor of Science in Nursing from Cedarville University.

Ashley decided to make a career change from her ten years within the healthcare industry as a pediatric emergency room nurse to retirement and 401K investment planning. She joined Victory Wealth Partners in 2008 after obtaining her Series 65 professional financial license and went on to earn her AIF (Accredited Investment Fiduciary) professional designation from the Center for Fiduciary Studies.