Monthly Archives: February 2020

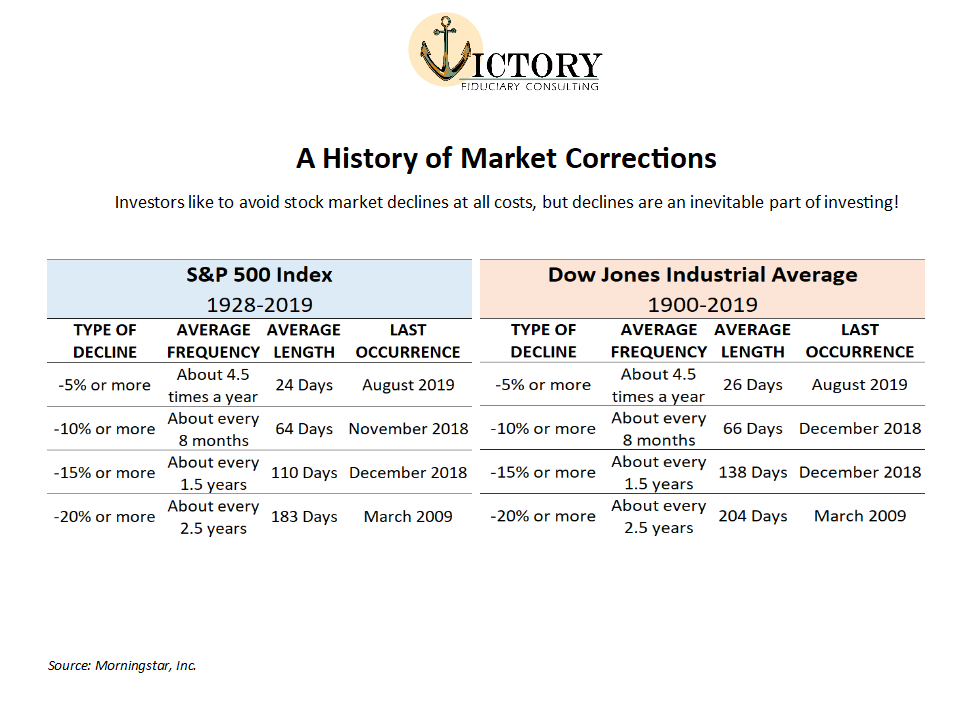

A History of Market Corrections

While the talking heads continue to stoke the flames of hysteria regarding the Novel Coronavirus, we would like to provide a follow-up to our previous article, “Do Global Flus Cause Market Blues”. If you have not read that article yet, we highly suggest you do. We discussed how recent volatility has seemed more pronounced due to an abnormally calm fourth quarter, as well as how the market has reacted to previous epidemics that have had a death toll of at least 100 people. As a recap, the market has averaged positive returns in the 90, 180, and 365-day periods following the initial outbreak, implying that there are other factors that have a much greater impact on the market. This time, however, we would like to discuss a phrase that is thrown around during times of volatility: market corrections.

In the same way a car’s engine can overheat, the stock market can overheat after periods of sustained and, more often than not, rapid growth. At the peak of these growth periods, stocks prices may have even increased faster than their actual underlying value. In these instances, the stock market typically enters a market correction. To put it simply, a market correction is a temporary resetting of market prices. Market corrections typically involve the market falling at least 10%, but they can even fall as much as 20%. In fact, the 2018 correction saw the S&P 500 index fall -19.78%. While no investor wants to see their account down 10%, market corrections are a vital and healthy aspect of our stock market.

As was previously mentioned, market corrections help to prevent the market from becoming egregiously overvalued. Just as the Federal Reserve adjusts interest rates to control inflation, market corrections act as a check on the stock market. While certain asset classes and sectors of the economy can go through isolated corrections, a market correction tends to affect all areas of the market at once. Once the market has seen a broad pullback amongst the sectors of the economy, stocks will once again continue their growth at their newfound prices. In short, market corrections help to ensure our stock market is at a healthy level and valuation.

Now that we have a better understanding of what a market correction entails, the next question is: when do they occur? Unfortunately, there is no crystal ball for predicting corrections. However, we can look at history to create realistic expectations of investing. In the two tables at the end of this piece, you will find a table each for the Dow Jones Industrial Average and the S&P 500, the two major U.S indices. The tables look at each index to observe the frequency of market pullbacks through history. In these tables, you will notice that pullbacks in the market are frequent throughout history. In fact, both indices have historically had a 10% or worse correction every 8 months! For perspective, the market has not had a correction of at least 10% since the end of 2018, meaning that, if history is to be our guide, we have been overdue for a correction. As of Thursday’s market close, we have surpassed the 7% pullback for the S&P 500 and 9% for the Dow Jones. While we can’t know for certain whether this will be closer to the pullbacks of the 2018 correction, we know that history shows us that corrections are a natural and relatively frequent occurrence in our markets.

Finally, the burning question on everyone’s mind: what should I do? While it is much easier said than done to stay the course during a correction, it is imperative that we remain diligent and long-term investors. We are reviewing the market and each asset class daily to see if there are any trend changes,

and we will make adjustments as needed. However, our six recession indicators remain positive, just as they did through the 2018 correction. If we observe any changes to these indicators, we’ll be sure to let you know. In the meantime, our best advice is to remain calm and stay informed. We will continue to do our best to provide you with relevant updates and information, but feel free to reach out to us if you have any questions or concerns.

Thank you,

Bud Verfaillie & Ashley Rosser

Victory Wealth Partners

Anchored in Compliance

53 N. Main St

Mullica Hill, NJ 08062

Office: 856-464-3100

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and not to be invested into directly.

The Standard & Poor’s 500 Index is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries. The Dow Jones Industrial Average Index is a price-weighted index of 30 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 30 stocks representing all major industries.

Is it Time to Leave Your Current Investment Holdings?

Do you know if it is time to leave your current investment holdings or even the stock market in general? Should I stay or should I go now? As the song goes “if I go it will be trouble but if I stay it could be double”. Of course I am not talking about relationships, rather I am referring to when you pull the trigger to sell your positions. Do you have a buy-sell discipline? Unfortunately for most investors, they do not have a formal process that determines if they should make major changes to their investment holdings. Rather, they make changes based on emotions or after something significant happens within the market. This is NOT a very good long-term strategy because unfortunately you are probably hurting your portfolio rather than helping it. Selling your holdings after they have gone down in value or buying positions after they have shot up in value are the equivalent of buying high and selling low. There can always be costs associated with mistiming both exiting and entering the market.

Don’t Leave your current investment holdings because of the nightly news

There is currently significant market volatility thanks to the corona virus outbreak. Many are wondering if this will have a long-term negative effect on their investments. As an Investment Committee, we conducted a study on the long-term effects of new disease outbreaks. We looked at the last 25 epidemics where at least 100 fatalities occurred, which took us back to the 1950’s. Most of the volatility was short-term, occurring in the first 60 days of each new event. If you would like a chart showing the specific epidemics and the volatility associated with specific periods, please contact us. Currently, we are not making any changes to our Investment Models. The stock market in general can be somewhat erratic, although if you have a sound investment management and screening process it can be more predictable that you may realize.

The investment strategy used by our firm, has a well-defined “buy-sell discipline”. This essentially means that there are very specific factors that help us determine when we should be in the market (versus investing in cash) as well as what specific areas of the market appear to offer the best opportunities. We will invest in areas of the market that show stronger performance momentum and conversely avoid areas with weaker momentum. All areas of the stock market will not be strong or weak at the same time. Wouldn’t it be nice to know what areas of the market are currently having strong or weak momentum BEFORE you invest? We decide what specific asset classes and sectors we include in our models based on how strong those areas are performing in current time. Many advisors employ a buy and hold method. They invest in the same asset classes over the long run. They make occasional FUND changes, but they do not change the underlying asset classes and sectors that comprise their portfolios. They periodically rebalance accounts to take from the areas that overgrew and give back to the areas that underperformed. We do not rebalance accounts, which essentially means take from the winners and give to the loser funds. Rather, we keep our models invested in the winners, until the momentum shifts and then we reallocate to a new area that is showing positive performance momentum. We keep our winners until they stop winning.

Only Leave your current investment holdings When ALL Major indicators point to sell.

The last and possibly most important distinction is we have a stop loss set up in our methodology that alerts us if we should consider leaving the market all together. We look at six distinct indicators and if four or more of those indicators turn negative, it is our sign that the stock market will not be the best opportunity for our clients and therefore we will move to cash until a majority of those indicators turn positive again. We will take what the markets will give us, and during the years the markets will be volatile and negative we are willing to be defensive to protect our client’s previous returns and principle. How desirable would it have been to have missed the vast majority of the 2008-2009 financial meltdown?

It is important as an investor to understand there are significant implications associated with both how your current portfolio is invested as well as timing when to get in or out of a specific asset class, sector, or the market in general. You should know if your advisor has a formal buy-sell discipline or they if use a buy and hold and rebalance method. You should also find out if there is a formal stop-loss discipline in place to alert if they should consider moving your account out of the market due to a significant downturn. If you are unsure, we would be happy to help you evaluate your current portfolio. It really is important to know “should you stay or should you go.”

Ashley Rosser, President

Ashley Rosser, President

Prior to her career in the financial services industry, Ashley earned her Bachelor of Science in Nursing from Cedarville University.

Ashley decided to make a career change from her ten years within the healthcare industry as a pediatric emergency room nurse to retirement and 401K investment planning. She joined Victory Wealth Partners in 2008 after obtaining her Series 65 professional financial license and went on to earn her AIF (Accredited Investment Fiduciary) professional designation from the Center for Fiduciary Studies.